PRIVATE CREDIT

An opportunistic strategy for income-focused investors

Our new private credit investment strategy capitalizes on the changed economic environment, offering some of the most attractive potential risk-adjusted returns of the past decade.

WHY PRIVATE CREDIT

A once-in-a-decade lending environment

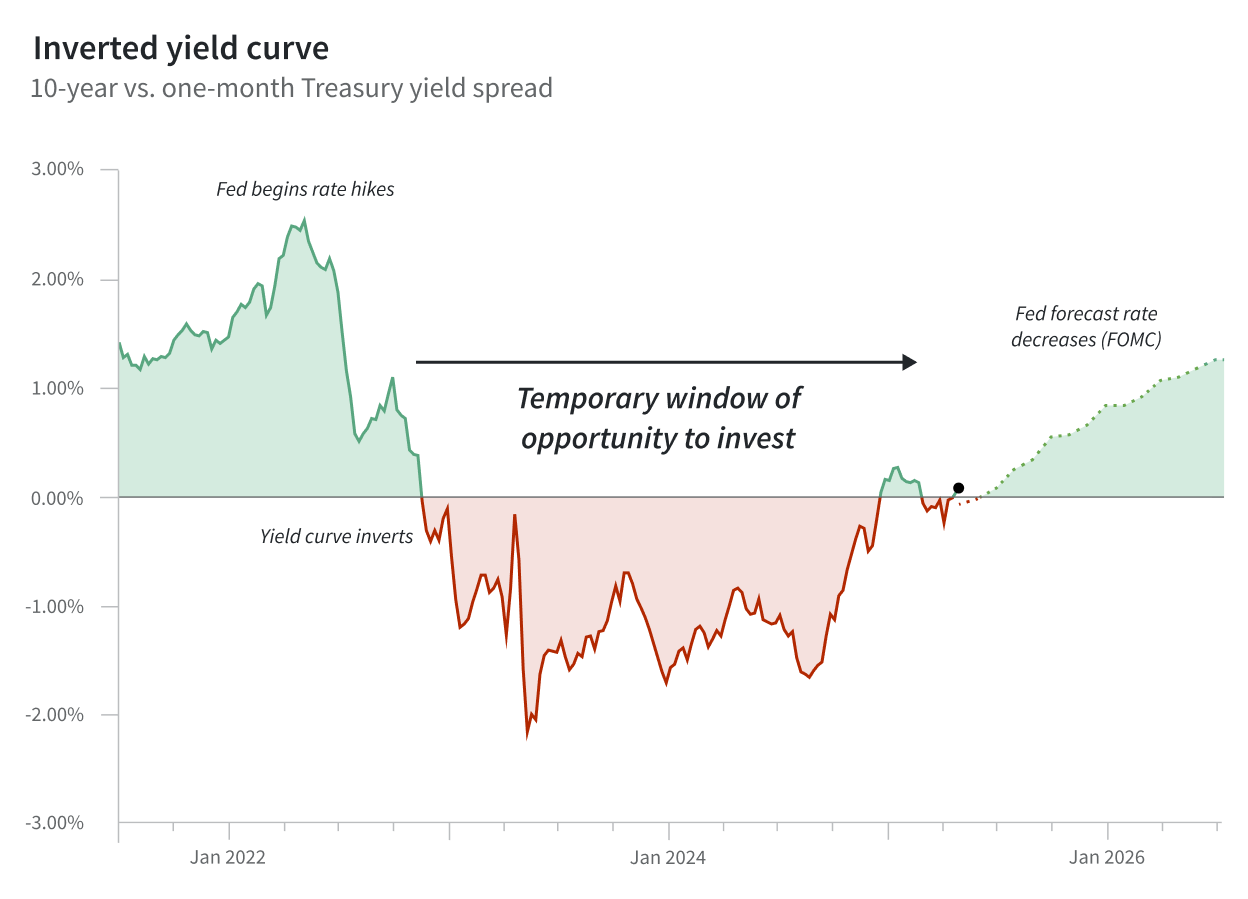

The Federal Reserve raised interest rates at record-breaking speeds in 2023 in an attempt to tame inflation. This policy shift has destabilized markets, leading to broad dislocations, increased strain across the system, and a potential liquidity crisis that presents a risk to the global economy.

Simultaneously, those factors have combined to create what we believe is arguably the most attractive environment for credit investments in a generation.

What is private credit?

Private credit (or private lending) is an asset class that consists generally of loans, fixed-income, or other structured investments that aim to deliver higher yields with lower overall risk when compared to equity investments. In other words, investors in private credit are lending money to borrowers in exchange for a fixed rate of return (often captured in the form of an interest rate or preferred return) but typically do not have any equity ownership or upside participation. Similar to other private market assets, private credit differs from publicly traded credit or fixed-income investments, such as bonds or asset-backed securities, because it is illiquid and consequently aims to deliver a higher relative return.

The profitability of preparation

As a result of the Fed's extraordinary actions, today it's more expensive to borrow money for 30 days than for 30 years. This is an unnatural state of affairs that we believe is creating a once-in-a-decade liquidity crunch that we're calling The Great Deleveraging.

During this period, individuals and companies seeking to borrow money, especially in the near term, will be forced to do so at significantly more favorable terms for investors. Higher interest rates will generally mean that borrowers will borrow at much lower leverage (which means lower risk). Virtually any loan maturing in 2023 will require a paydown, and for new loans the gap between the expected and actual proceeds will likely require the use of “bridge” or “mezzanine” financing.

Meanwhile, investors who have been diligent and chose to maintain larger cash positions over the past few years will be in the enviable position of being able to demand significantly more return in exchange for providing liquidity during what we expect is likely to be a temporary period of realignment. FNTVS is in that position.

Important Note: In our experience, these types of unique investing environments are short-lived. Accordingly, our expectation is that the current period of disruption is unlikely to last beyond 2024.

Source: Historical Treasury rates sourced from St. Louis Federal Reserve Economic Data (FRED). Forecast based on FOMC projections for the Fed Funds rate and FNTVS internal analysis of Treasury spread behavior from historical yield curve inversion events.

Our Track Record

Billion-dollar experience

While this strategy is newly calibrated for this environment, we’re able to draw on a deep well of executional experience. Since 2012, we've acquired or financed over 10,000 residential units and have made more than 50 unique mezzanine and preferred equity investments in real estate.

$135 million

Capital Deployed into Debt Projects

120+

# of Deals

20k+

Active Investors

12.0%

Since 2020

Featured Fund

Income Real Estate Fund

A diversified credit fund focused on real estate debt investments across prime markets. Our strategy involves providing financing for residential and commercial developments.

8.5%

Target Annual Return

$100M

Total Fund Size

8.5%

Expected Yield

Asset Types

- Homebuilder finance

- Real estate debt

- Preferred equity

- Public REIT equities

- Multifamily

Example Project

Waypoint

As part of our new private credit strategy, we've invested roughly $20.8 million to provide financing in the form of preferred equity for the development of the Mason at Daytona Beach, a 300-unit multifamily community on 65.4 acres of centrally located land in Daytona Beach, Florida. Under the terms of the investment agreement, the borrower has agreed to pay us a 13.5% fixed annual rate that will accrue for as long as it takes to finish the project, and our investment will be paid back upon its completion. This is one of many projects in the Income Fund's Portfolio.

About Our Strategy

Market dislocation creates opportunity

The opportunities created by the Great Deleveraging era are clear: the sudden need for sponsors and new asset capital offers a critical window for investors. What’s less obvious, but equally important, is how you act during this short-term period. For those who are sufficiently prepared, the next 12–18 months could be one of the greatest periods to invest in decades. But, if you miss the moment, you may never see this kind of opportunity again.

The dislocation in real estate credit markets has created opportunities that, regardless of the quality of underlying credit, are not known and have not yet been corrected. Our goal is to deploy capital into these areas while others are moving capital into cash or other ‘safe haven’ assets.

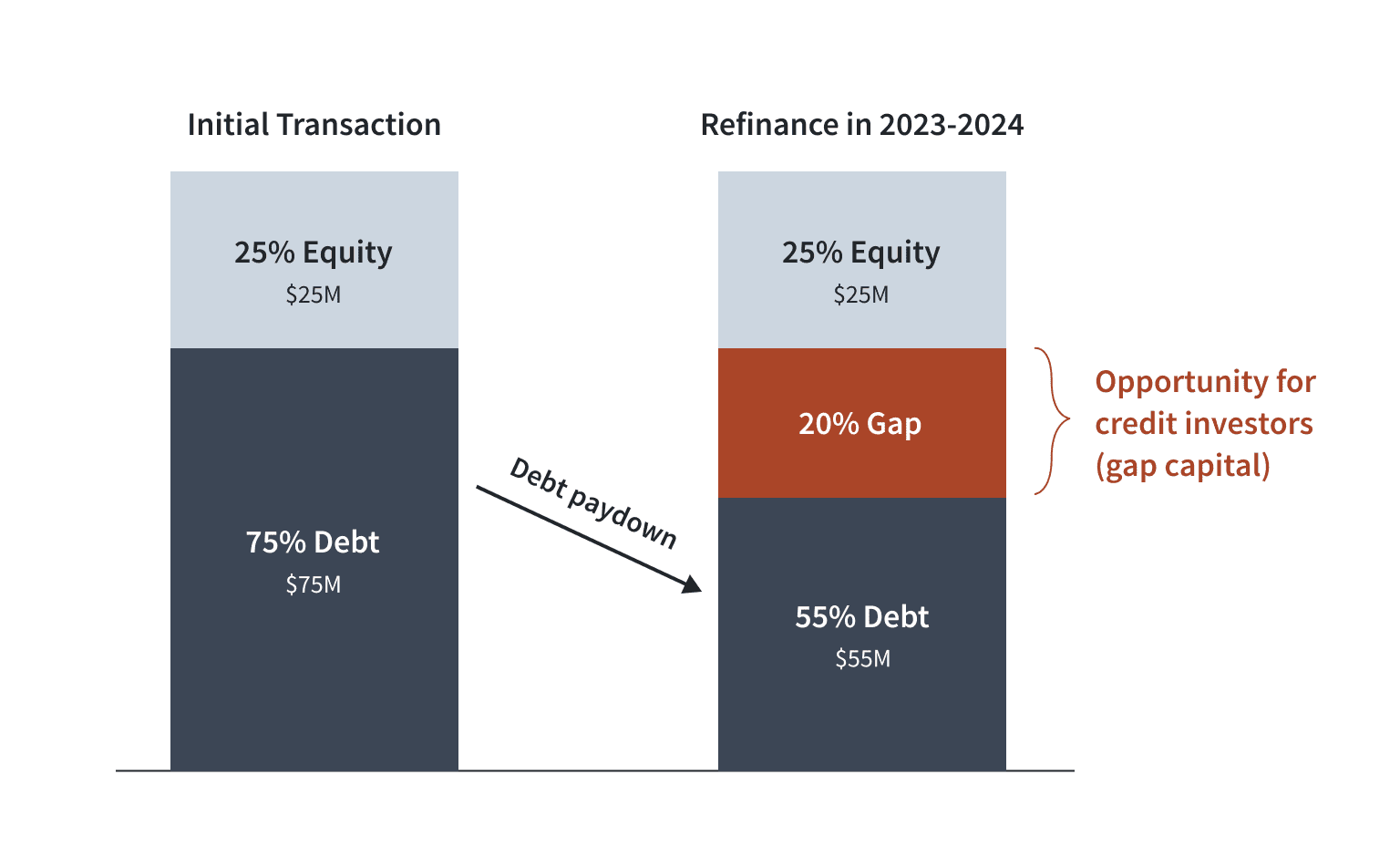

Funding the gap

By stepping into the gap, we can provide critical financing to assets and borrowers that need liquidity, while capturing attractive risk-adjusted returns. Between 2023 and 2024, we expect to focus our resources on filling this gap and generating meaningful returns for our investors.

Examples of this kind of activity include:

- Originating or restructuring senior loans, including senior mortgage loans and development financing.

- Providing mezzanine financing for preferred equity, debt, or bridge loans.

- Sourcing the rescue or preferred financing for GSE (e.g., Fannie Mae or Freddie Mac).

- Financing residential construction and development.

- Acquiring abandoned assets and high-yield investments in the most backed securities markets.

Initial Transaction vs. Refinanced (2023–2024)

Explore all projects in our portfolio

Here are the investments that are powering our investors' returns.

Viewing 6 of 6 assets

Invest in Private Credit

Access consistent income through carefully structured credit investments with rigorous underwriting and active portfolio management.